Last week the ONS published its latest labour market update. These figures show that it is a fantastic time to be looking for work, vacancies are near to a record high and companies are raising pay to help them attract staff. It is important to note that we are not back at the levels we saw before the pandemic, and the number of people not in work and not looking for work is still high.

Companies are struggling with labour and skills shortages which will constrain economic growth in the long term. We don’t have to look far for evidence that labour shortages have the power to bring segments of the UK economy to chaos. We only have to look at recent incidents in airports, driver shortages and NHS waiting lists growing.

This is the primary reason why I am working incredibly hard and closely with our current clients to overcome these shortages and get the UK economy growing strongly again.

To do this though, both business and government must bring workforce planning (more importantly for me sales force planning) to the front of their minds. Businesses must think very differently about how they hire, upskill and treat their staff. There is an argument for companies to create intern schemes and training incubators to assist with skill development.

Unemployment rate

Latest figures:

- 3.8% in Mar-May 2022, down by 0.1% from the previous quarter, and 0.2% since before the pandemic (ONS)

Projections:

- 4.0% in Q4 of 2022 (Office for Budget Responsibility)

- Unemployment is expected to rise to 5.0% by 2025 (BoE)

CPI inflation

Latest figures:

- CPI 12-month rate was 9.1% in May 2022, up from 9.0% in April 2022.

- CPI Index was 120.8 in May, up from 120.0 in April.

Projections:

- CPI inflation is expected to rise further over the remainder of the year, to just over 9% in 2022 Q2 and averaging slightly over 10% at its peak in 2022 Q4 (Bank of England).

- CPI Inflation is expected to peak at 8.7% in Q4 2022 after another increase in the energy price cap in October (OBR).

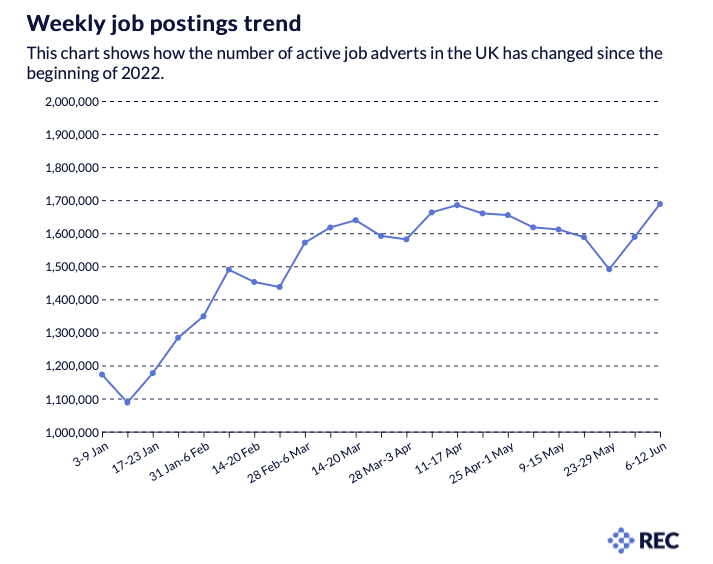

Vacancies

- There were 1,294,000 vacancies from Apr-Jun 2022; a small increase of 6,900. This was also 498,400 above its pre-pandemic levels (Jan-Mar 2020).

- The largest quarterly increase in vacancy number was in accommodation and food service activities (+10,200), but this was offset by falls in other industry sectors, most notably wholesale and retail trade; repair of motor vehicles and motorcycles (-7,200).

The crucial element to what we are experiencing now is that the pandemic has just shone a light on an inevitable issue that has been facing us for years. As the “baby boomers” retire, the inefficiencies in our skills system become apparent; this was always going to make this decade challenging. Government intervention and a robust labour market strategy are vital. Skills are hugely important, as well as immigration and infrastructure.

“With a 10% surge in demand for staff across the economy, and the labour market restricted by shortages, we could see a 1.2% fall in expected GDP and productivity by 2027 – costing the economy anywhere between £30 billion and £39 billion every year.” (REC)

Neither government nor business can do this alone. It’s time for both to get the “people strategy” right and get serious about long-term workforce planning, investing in a skills pipeline, and giving recruitment the importance it deserves.

REC’s recommendations include the following;

1. Aim to have a 5-year workforce strategy and investment plan

2. Improve training and development opportunities for all staff

3. Implement equality, diversity and inclusion policies

4. Improve staff engagement, actively listening to staff and deploying a range of tools to retain talent

As we close out July and schools break up, I wish you a wonderful Summer.

Although it’s time to think long and hard about your workforce planning, we have to make time for quality time with family and friends. There is something so special about the long days and lighter evenings.

See you in September for another recruitment update.